One takeaway a day, for the week

For those who unfortunately missed Seyna's live stream on 13 November, here are seven lessons to remember, one per day, to make the most of your week!

For a long time now, health insurance has been said to be in ‘crisis’.

It's a word that comes up often, too often, in conversations between insurers, reinsurers and brokers.

Declining profitability, regulatory pressure, delisting of drugs and treatments, portfolio volatility: there is no shortage of challenges in health insurance!

But as is often the case, it is in times of uncertainty that the most innovative players emerge.

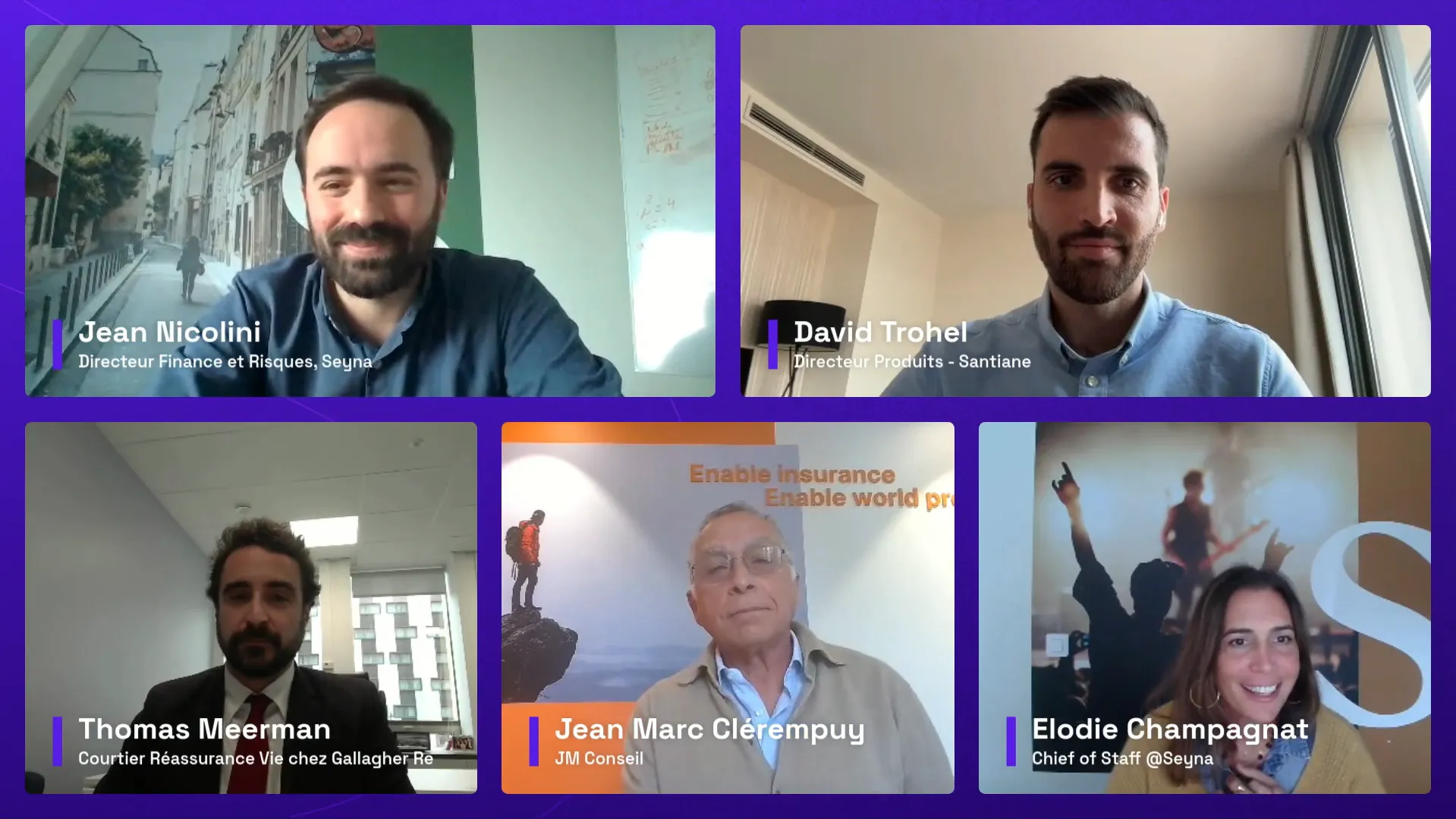

This is the whole point of the latest Seyna Live, where four experts, David Trohel (Santiane Group), Thomas Meerman (Gallagher Re), Jean-Marc Clérempuy (consultant and former CEO of CEGEMA) and Jean Nicolini (Seyna), shared their different perspectives on the market and offered numerous insights.

For those who unfortunately missed the event, here are seven lessons to take away, one per day to make the most of your week!

Monday – A tense market, but still lively

Health insurance is a demanding market.

Historically, profitability is achieved after three years of marketing, when everything goes well...

But in recent years, between revaluations, new taxes and changes to the 100% healthcare scheme, the equation has become more complex.

For David Trohel, the key lies in agility: knowing how to adjust your offerings quickly, controlling your time-to-market, and relying on solid partnerships.

For Jean-Marc Clérempuy, it is necessary to ‘restore the balance between what the consumer wants, what the risk bearer offers and what the broker distributes’.

In other words: a return to common sense in insurance.

Tuesday - Better monitoring, earlier

Everyone agrees on one thing: health insurance should no longer be managed blindly.

Gone are the days of waiting three years to draw conclusions about a product.

Jean Nicolini reiterated this point: "At Seyna, we don't share the fatalistic view of health insurance, but we don't kid ourselves either. We need to monitor the data from the very first months, make adjustments early on and act quickly."

Risk management also requires joint oversight between brokers, insurers and reinsurers. Thomas Meerman considers this alignment essential to restoring confidence and profitability.

Wednesday - The success of 'non-regulated' health insurance products

This is the paradox of the moment: ‘non-regulated’ products, long perceived as marginal, have become a lever for profitability.

These are ‘low-end’ products, with adjusted guarantees, more accessible rates and solid technical results.

For Jean-Marc Clérempuy, a staunch defender of non-regulated insurance, it is a ‘fairer and better managed offering’.

And the figures prove him right: many non-regulated portfolios held by our partner brokers are now outperforming traditional regulated contracts. Even if not everything about regulated contracts is to be discarded.

This trend simply shows that innovation does not always come from the top (increased coverage and complexity), but sometimes from simplification and, above all, from the reality on the ground.

Thursday - Pooling resources for greater sustainability

Another important lesson: profitability in health insurance is not achieved on a product-by-product basis.

It is built on a global portfolio approach.

Combining health insurance with life & disability insurance, accident coverage or pet insurance makes it possible to spread risks, cushion technical deviations and build customer loyalty more easily.

This approach is used by all players, from the placement of risks with reinsurers to the choice of cross-sell products offered to customers by brokers.

‘Rather than waiting three years to break even, let's see which products can secure margins sooner,’ suggests Jean Nicolini.

Friday - Customer loyalty, the key to success

Because profitability is worthless without customer loyalty.

For Jean-Marc Clérempuy, the recipe is simple:

- Choose your manager carefully.

- Treat complaints seriously.

- Train your teams to speak the same language as your policyholders.

‘You rarely lose a customer because of the product. You often lose them because of silence.’

A phrase to ponder.

Saturday - No innovation without quality execution

The future of health insurance will depend on a coordinated evolution between innovation, management and quality of execution.

For David Trohel, differentiation will come as much from the offering as from operations:

‘In a competitive market, we need to get back to basics: clean management, smooth customer relations and stable offerings. That's also where profitability comes into play.’

In other words, innovation only has an impact if it is backed by flawless execution.

Sunday - Reinsurance, the technical co-pilot

On the reinsurance side, Thomas Meerman sees the future in long-term partnerships that are better structured and more transparent:

‘To make progress in health insurance, we need to move away from short-term thinking. With multi-year agreements and regular data sharing, we can manage things much more calmly.’

The reinsurer thus becomes a technical co-pilot, providing benchmarks, risk assessments and the necessary adjustments to ensure economic stability.

Conclusion: what does the future hold?

Health insurance is not in crisis.

Tomorrow, health insurance could take inspiration from affinity insurance: more agile, modular products that are continuously adjusted using data.

Those players who are able to adapt, cooperate and innovate without naivety will emerge stronger from this period.

And that is exactly what we like to see at Seyna: clear-headed players who remain optimistic!